Medicare Supplement Plans (also referred to as Medigap) are insurance policies designed to provide coverage for some of the costs that Original Medicare doesn’t cover.

Note: We will be using the terms “Medigap” interchangeably with Medicare Supplement – they refer to the same thing.

- Am I Eligible For A Medicare Supplement?

- Medigap For Folks Under 65

- What Do Medicare Supplement Plans Cover?

- What Plans Are Available?

- Plan F

- Plan G

- Plan N

- Medigap Plan D

- Other Medigap Plans

- What Plan Is Best For Me?

- What Do Plans Cost?

- How To Choose The Right Plan?

- Medicare Supplement vs. Medicare Advantage Plans

- Drug Coverage

- When To Sign Up

Doctor visits, hospital stays, skilled nursing, home health care, and durable medical equipment are some things these plans will help cover.

Medigap plans are available to purchase from private insurance companies. The U.S. Government regulates the plan benefits, insurance companies are required to offer the same policy, but they can charge different premiums. The plans are “standardized.”

To illustrate this, Cigna and Aetna both sell Medicare Supplement Plan G. Aetna may charge $100 per month, and Cigna’s plan may cost $115 per month. Both companies are required to offer the same benefits but can charge different premiums for it.

Am I Eligible For A Medicare Supplement?

To be eligible, you must have both Medicare Part A and Part B. The supplement plan pays AFTER Medicare approves and processes the claim.

Medigap For Folks Under 65

Medigap plans are available to most folks under 65 as long as they have Medicare A+B. In certain states, insurance companies are not required to offer Medigap plans to people under 65. Also, the price can be substantially higher when you are under 65 in some areas.

If you are under 65 and eligible for Medicare Parts A & B, call us at 800-208-4974 to find out what a Medicare Supplement plan would cost.

In certain situations, a Medicare Advantage plan can make sense due to the high cost of a Medigap plan for people under 65.

What Do Medicare Supplement Plans Cover?

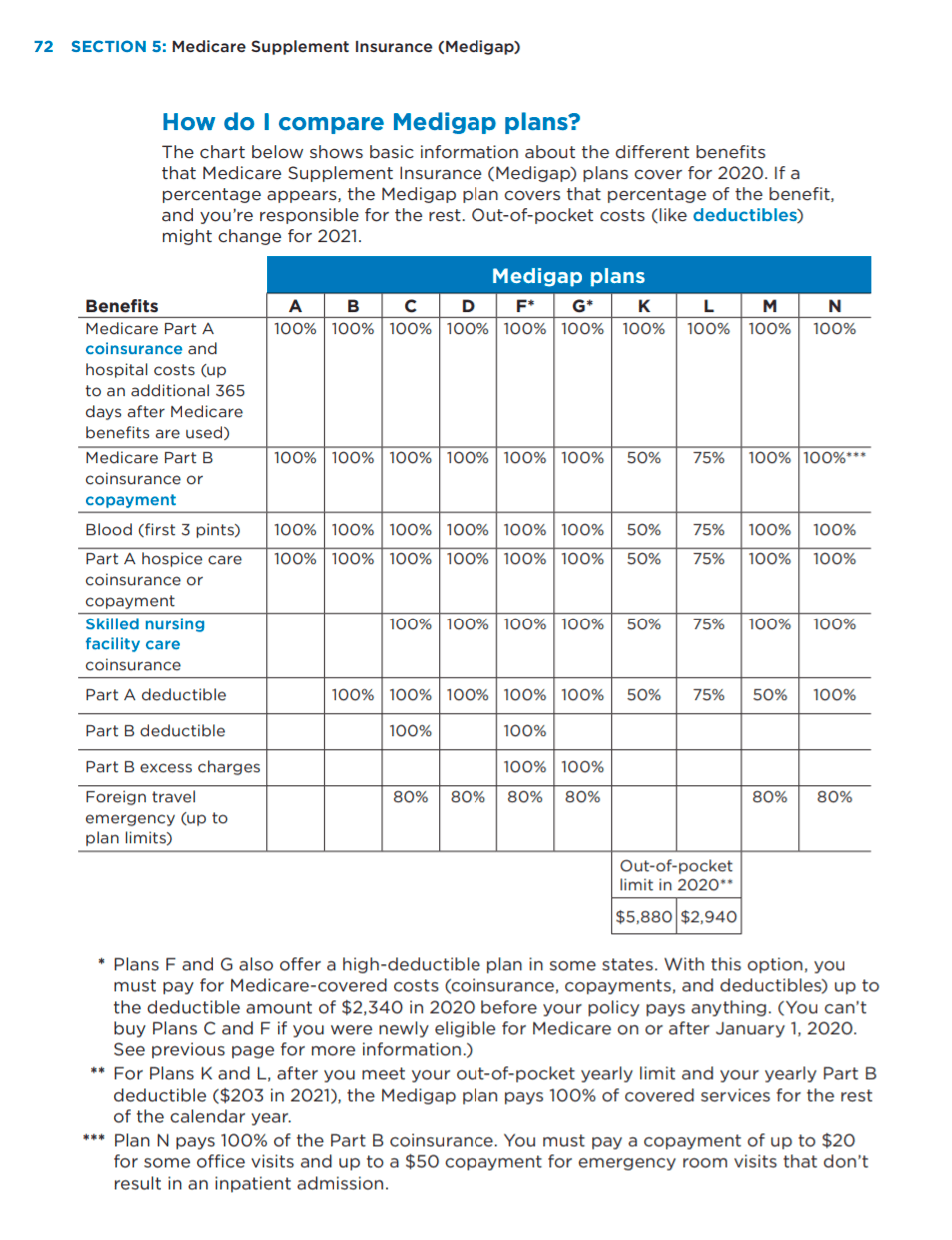

Medigap plans will cover the “gaps” leftover from Original Medicare. Medicare alone has many out-of-pocket costs; below is a chart taken from the Medicare and You Guidebook.

Read more about what Original Medicare covers here.

Medicare Supplement plans only cover services that are approved by Medicare. The supplemental is secondary to Medicare. If Medicare doesn’t approve your claim, then the Supplement plan will not pay.

What Plans Are Available?

In most states, there are 10 Medigap plans available for purchase; each plan provides a different level of coverage.

Plans are labeled A, B, C, D, F, G, K, L, M, and N (Plans E, H, I, and J are no longer available). Medigap policies are standardized differently in Massachusetts, Minnesota, and Wisconsin.

Plan F

Plan F is the most comprehensive plan available. This plan provides 100% coverage for all Medicare eligible services.

Up until January 1st, 2020, Plan F was available to all Medicare beneficiaries. In 2018 Plans F and C were eliminated as options to newly eligible Medicare beneficiaries. If you started Medicare Part A before Jan 1st, 2020 you can still buy Plan F.

Read more about Plan F here.

Plan G

Medicare Supplement Plan G is currently the most popular plan available. This plan provides the same coverage as Plan F with one exception; the Medicare Part B deductible.

Medicare Part B Deductible

This deductible is $240 in 2024. Beneficiaries are responsible for paying this deductible at the doctor’s office, once per year. It often takes folks a few doctor visits to reach the $240. Once you have paid this amount, you have 100% full coverage.

Read more about Plan G here.

Plan N

Plan N is becoming more popular, mainly because Plan F is no longer an option for folks new to Medicare. This Plan provides similar coverage to Plan G with a few exceptions:

- The Part B deductible is not covered (same as Plan G).

- $0-$20 copayments at office visits.

- $50 copayment at the emergency room (waived if admitted).

- Part B Excess charges are not covered.

To read our detailed Plan N article, click here.

Medigap Plan D

Medigap Plan D is similar to Plan G. The only difference is that Plan G covers the Part B Excess Charges and Plan D does not.

Other Medigap Plans

We have reviewed plans F, G, and N. There are still seven other Medigap plans we haven’t covered. These plans aren’t as popular because they don’t offer the same level of coverage. Also, the prices of these plans generally do not justify the benefits.

For example, you can purchase a Plan N for less than the amount it would cost to buy a Plan L. Plan N provides a much richer level of coverage, with a lower price tag. No brainer, right?

If you want to learn more about these plans, continue reading our article about “the other” Medigap plans here.

High Deductible Plans

For those folks who want protection against potential large hospital bills but want a low premium may opt for a high deductible plan.

There are two high deductible Medigap plans to choose from:

- High deductible Plan F

- High deductible Plan G

These are just versions of regular Plan F and G with a deductible added. The deductible for 2024 is $2,800 . Policyholders of these plans must meet the full deductible before their supplement beings to pay claims.

Agent Tip

The same rules apply to the high deductible version of Plan F; Medicare beneficiaries who turned 65 or started Part A after January 1st, 2020, are not able to purchase it. Instead, they can buy High deductible Plan G.

What Plan Is Best For Me?

Individual needs vary from person to person. For this reason, it is essential to review your personal needs and expectations for a plan.

Check out our detailed review on the best plans and companies for 2024.

We can help you navigate the confusing maze of Medicare options. Just give us a call at 800-208-4974 today.

What Do Plans Cost?

Prices vary depending on location, age, and company. The cost can range significantly between carriers for the same plan letter. Generally, Plan F is the most expensive of the three plans, followed by Plan G. Plan N is the most affordable.

View instant rates using our online quoting tool here.

Do Prices Go Up Over Time?

Yes, the rates do increase over time. The plans are priced in one of three ways:

Community Rated – With these plans, the base premium is priced the same for everyone in the area, regardless of age. You’re premium may go up due to inflation or other factors, but not due to age.

Age-Attained – With an age-attained policy, the carrier will price the policy based on your age at issue, and the premium will increase over time due to your age.

Issue-Age – The premium is based on your age at issue and the premium will only increase due to factors such as inflation. You’re premium will not go up due to age.

How To Choose The Right Plan?

Does It Matter What Insurance Company I Choose?

We talked about how the benefits of the same plan letter are identical between companies. So you might be asking yourself, “well, shouldn’t I just choose the lowest price?”

Even though the coverage is the same between companies for the same plan, there are several important factors to consider when comparing carrier options.

Continue Reading: Medigap Insurance Carrier Reviews

Medicare Supplement vs. Medicare Advantage Plans

Advantage plans and Medigap plans work very differently.

Advantage plans come with a network of doctors and hospitals you must stay within. Also, there are many copays and deductibles with Advantage plans.

The “advantage” is the monthly price is usually less than a Medigap plan. Medicare Advantage plans generally include drug coverage.

Medigap plans are “portable,” meaning they allow you to use any Medicare doctor or hospital, anywhere in the country, without needing a referral.

At Bluewave Insurance, we offer both Medigap and Medicare Advantage plans.

Drug Coverage

Medicare Supplement plans do not include drug coverage. If you purchase a Medigap plan, you would have to buy drug coverage separately. “Part D” is the term commonly used to reference drug plans.

Agent Tip

There is a penalty for not signing up for a Part D plan when you are the first eligible. The penalty amount is calculated by the number of months you went without a Part D plan. You pay the penalty for life.

We highly recommend purchasing a Part D plan if you enroll in a Medigap plan. Contact us if you have any questions about Part D.

When To Sign Up

The best time to sign up for a Medicare Supplement Plan is when you are new to Medicare or turning 65. This period is “Open Enrollment.”

Open Enrollment for Medigap starts the first of the month you turn 65 or start Medicare Part B and lasts for six months. During this period, you can choose any plan you want, and you are NOT subject to any health questions.

Considerations When Making Changes

If you currently have a Medigap plan in place, you can make a change to a different Medigap plan or company anytime throughout the year. You may be subject to health underwriting questions, and you can be denied acceptance due to health.

Call us today to review options at 800-208-4974.